Coronavirus Paid Leave: How Employers Can Get Reimbursed in 3 Steps

3 steps that employers should follow to cover their losses due to COVID-19, and ensure job protection for their employees

April 3rd, 2020

The Coronavirus pandemic has resulted in losses amounting to billions of dollars in the last three months. This is due to a number of factors – a lack of running businesses and a sharp decline in employee activity being the two primary culprits. The latter also brings out the coronavirus paid leave crisis, which is causing greater economic damage to enterprises than anything else.

According to one estimate, the five biggest technology companies dropped over $400 billion in value since January. This, compounded by massive restrictions on the global workforce, has left both employers and employees in uncertain conditions.

The U.S. government has made provisions for employees under a new law called the United States Families First Coronavirus Response Act (FFCRA), passed by President Trump.

But what can employers do to cover their losses (and ensure job protection for their full-time employees) in light of this public health emergency?

Let’s get right into it.

Coronavirus Paid Leave Provisions for Employers

The extended medical and family leave provisions (and individual paid medical leaves) apply to a number of private and public employers.

Here is the eligibility criteria for employers to qualify for this provision:

Employers must be either a public or private business

They should have fewer than 500 employees at the time of application

They should already provide ‘qualified sick leave wages’ (as required under the Families First Act)

They should already provide ‘family leave wages’

In addition, small businesses with fewer than 50 employees can qualify to be exempted from the requirement under the Act to provide paid leave for child care unavailability or school closings, or to provide care to a family member in self-quarantine, in case a health care provider is not available.

This is in case the leave requirements would impact the profitability of the business as an on-going concern.

Coronavirus Paid Leave Tax Credits for Employers

As per the Families First Act provisions for employers, the U.S. Department of Labor (DOL) and the Internal Revenue Service (IRS) provides eligible businesses with tax credits to cover the cost of sending employees away on paid sick leaves.

These tax credits are applicable from April 1st, 2020, through December 31st, 2020.

The number of refundable tax credits under the Act, are as follows:

Up to 100 percent of the total amount paid for up to 10 days of qualified sick leave (ESPL) wages

Up to 10 weeks of qualified family leave (EFMLA) wages

Any qualified healthcare plan expenses that can be allocated to those wages

The amount of the eligible employer’s share of any and all Medicare taxes applicable to those wages

For official rules and regulations regarding the Families First Act’s paid sick leave and expanded family leave entitlements, click here.

Sick Leave Credit Amount

Eligible employers can receive a refundable sick leave credit at their employees’ regular rate of pay, up to $5,110 in the aggregate, and $511 per day, for a total of 10 days.

There are currently no provisions in regard to paid family leaves for part-time employees.

Child Care Leave Credit Amount

In case an employer needs leave to care for a child whose place of care and/or school is closed, or if there is a lack of adequate support from a child care provider due to the coronavirus, they can receive up to $10,000 in the aggregate, or up to two-thirds of the concerned employee’s regular pay.

The latter amount is capped at $200 per day, for up to 10 full days.

How to Claim Coronavirus Paid Leave Tax Credits in 3 Steps

Here’s how you can claim the refundable tax credits on all paid leave wages during the applicable period.

1. Compile a Report on Leave Wages

Eligible employers should, first and foremost, compile a report on their total qualified leave wages for each quarter, on their federal employment tax returns.

This includes all the leaves currently taken by the employees, and the remaining ones for the quarter in question (through December 31st, 2020).

2. Report Related Credits

After they have calculated their total qualified leave wages for the quarter, employers need to calculate the related tax credits (according to the amount percentage mentioned earlier).

3. File Form 941

Form 941 is used to report the income, social security, and Medicare taxes that the employer withholds from employee wages.

It also reports the employer’s share of Medicare tax and social security payout. Employers should file and submit Form 941 at the earliest (for the applicable quarter), using the Federal E-File facility.

Employers can also mail the completed Form 941 to their state’s Department of the Treasury Internal Revenue Service office.

Obtaining an Advance on Refundable Tax Credits

Certain eligible employers can also fund the qualified leave wages by accessing their federal employment taxes, which include their withheld taxes, all of which they would need to deposit with the IRS.

Employers can do this in anticipation of receiving their due tax credits. Furthermore, they can request an advance on their tax credits from the IRS.

The IRS presents this provision because quarterly returns are not filed until the employer is required to pay the qualified leave wages. The employer may not have a sufficient federal employment tax amount set aside to fund the required qualified leave wages.

To combat this issue, the IRS has created a procedure for employers to obtain an advance on their refundable tax credits.

Here’s how qualified employers can apply for an advance on their credits:

1. Reduce Quarterly Tax Deposits

First, eligible employers will need to reduce all remaining federal employment tax deposits (applicable on wages paid within the same quarter) to zero.

2. File Form 7200

In case the allowed reduction in deposits is not equal to the qualified leave wages, eligible employers can file Form 7200, Advance Payment of Employer Credits Due to COVID-19.

Filing this form will let them claim an advance on their credits for the remaining qualified leave wages that it paid out within a quarter, for which the employer didn’t have enough federal employment tax deposits.

Key Takeaways from the Families First Coronavirus Response Act

Here are some of the biggest takeaways from the Coronavirus paid leave provisions i.e. the Families First Act (FFCRA).

Complete Coverage for Employers

In accordance with the policies highlighted within the Act, employers can receive 100% reimbursement on all their paid leave wages.

Health insurance costs are also included in the tax credits. Furthermore, qualified employers will face no liability on the payroll tax.

Even self-employed individuals can receive similar tax credits.

Quick Funds

The IRS is working to provide immediate reimbursement, upon the filing of the required tax forms. This makes the tax credit reimbursement easy and quick to obtain.

The IRS is also providing a fast dollar-for-dollar tax offset against the payroll taxes.

In case a refund is owed (upon filing), the IRS will submit the funds as soon as possible.

Note: The IRS has not provided an official ETA on the submission of the refund amount(s). Refund submission times may vary for individual employers.

Protection for Small Businesses

Employers who run very small businesses (fewer than 50 employees) can also apply to be exempt from being required to provide paid leaves.

However, these exemptions will only apply for leaves due to caring for a child whose school is closed, or in case adequate childcare is not available, both in cases where the business’s viability may be threatened.

Leniency in Compliance

If required, businesses can simply take out the funds that they would have otherwise paid to the IRS in federal payroll taxes, and use them as tax credits.

In case those amounts are not enough to cover the total cost of paid leave, employers can also apply for an expedited advance from the IRS.

For this, they will be required to submit a simple claim form (to be released).

Under this particular policy, there was a 30-day non-enforcement period for employers making good-faith compliance efforts. The DOL did not take action against employers who were found in violation of the Act, from March 18 through April 17, 2020, as long as the employer had acted in good faith and tried their best to comply.

During this 30-day period, the DOL started to assist the employers with compliance, instead of building a case against them.

Final Word

Any and all tax credits under the Families First Coronavirus Response Act are subject to qualification through the IRS and the DOL.

As such, it’s important to dot all the I’s and cross all the T’s, when filing for credits.

This is to make sure you receive the reimbursement amount on time, and your employees can stay safe within their homes, without fear of financial hardship.

Filing for tax credits is easier said than done though, especially for companies who are already struggling with numerous other employee matters and paperwork. This requires a specialized Time Tracking and PTO Management Software, such as the one provided by GoCo.

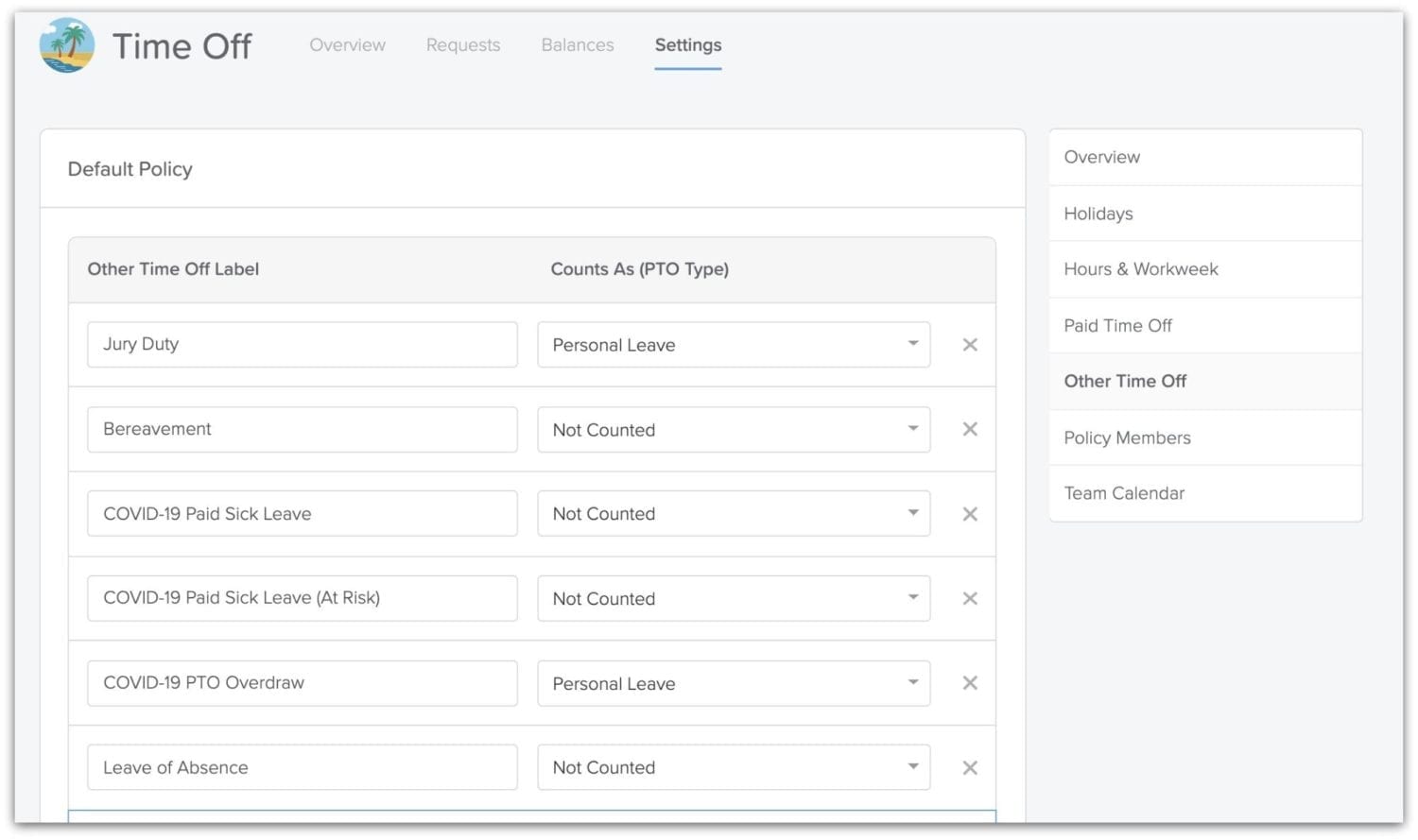

Here’s one example of how we helped track a client’s employee leaves, according to the policies defined in the Act: GoCo can assist you with remote work planning for COVID-19, as well as, maintaining a stable HR framework through the crisis via our range of software tools and Coronavirus-specific resources.

GoCo can assist you with remote work planning for COVID-19, as well as, maintaining a stable HR framework through the crisis via our range of software tools and Coronavirus-specific resources.

To learn more about how we can assist your company come to grips with the pandemic on the HR front, schedule a free demo today.

Subscribe to Beyond The Desk to get insights, important dates, and a healthy dose of HR fun straight to your inbox.

Subscribe hereRecommended Posts

Top 5 Mistakes of Overworked HR Departments

Blog Articles

Search...

Product

GoCo

Resources

Articles

eBooks

Webinars

Customer Stories